Hewlett-Packard

Inside the Business of HP

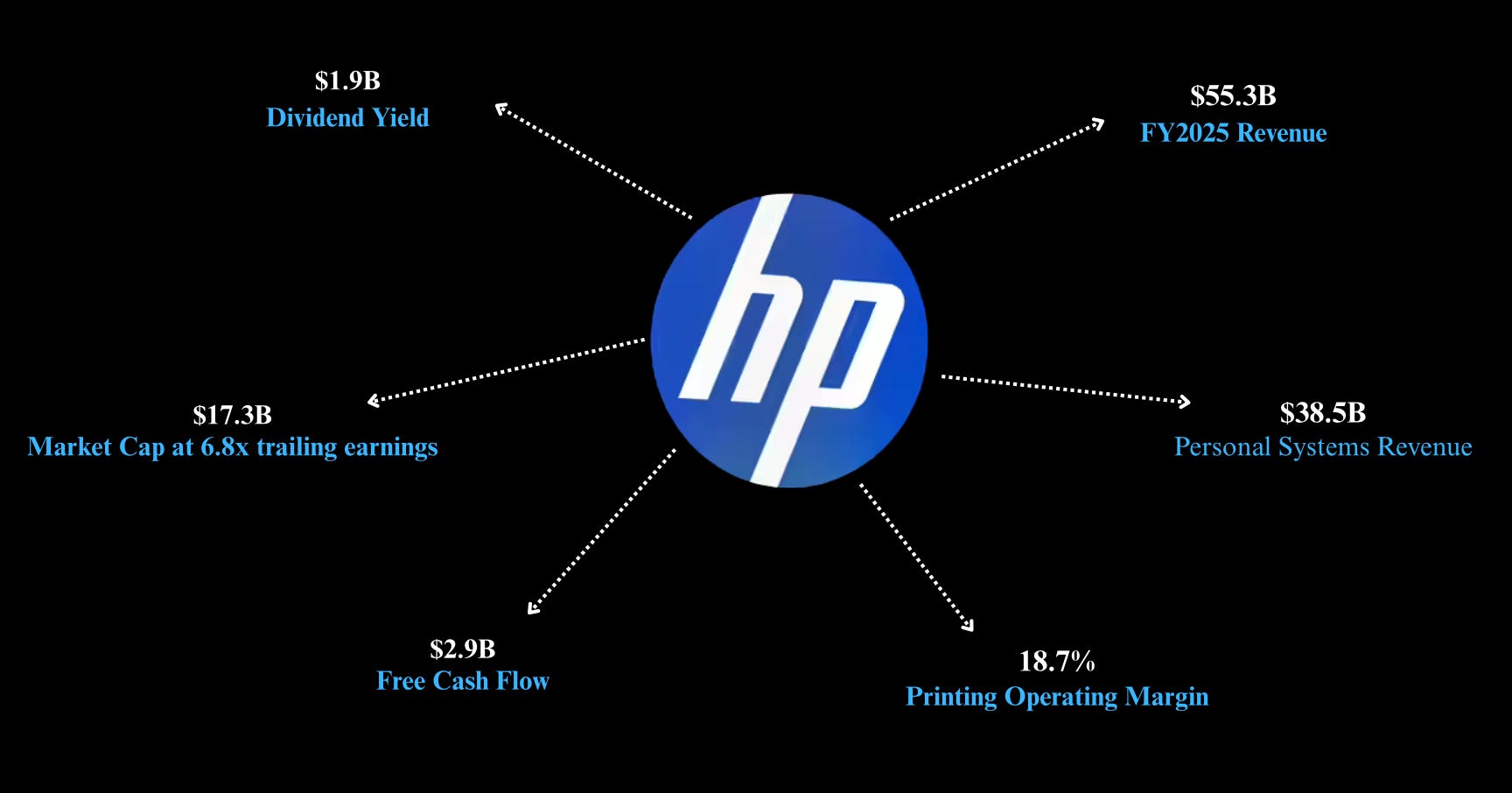

HP does about $55 billion in annual revenue, yet the market is pricing it like a business in distress. It’s trading at just 6.8x earnings, with a free cash flow yield north of 16%, numbers you’d normally associate with something fundamentally broken.

The reality is more nuanced. A mix of factors has weighed on sentiment: the CEO’s departure, a steady decline in the printing business, margin pressure from rising memory costs and tariffs, and a broader market shift that’s aggressively rewarding companies with a clear AI infrastructure story. HP doesn’t quite fit that narrative.

The stock reflects that disconnect. It dropped 29% through 2025 and is down another 9% so far in 2026. Over the same stretch, Dell Technologies has surged 51%, largely on the back of a $43 billion AI server backlog that positions it squarely in the market’s current sweet spot.

Operationally, HP is still very much relevant. It holds around 21% of the global PC market, second only to Lenovo at 25%, and remains the clear leader in printers with roughly 34% share. It also generates about $2.9 billion in annual free cash flow, most of which is returned to shareholders.

So the real question isn’t whether HP is a large, functioning business, it clearly is. The question is whether it can manage through the structural decline in printing, the ongoing commoditisation of PCs, and a leadership transition, well enough to justify the massive valuation gap between its roughly $17 billion market cap and Dell’s $117 billion.

That’s the lens this analysis is built around.

1. Company baseline: FY2025 financials and operating detail

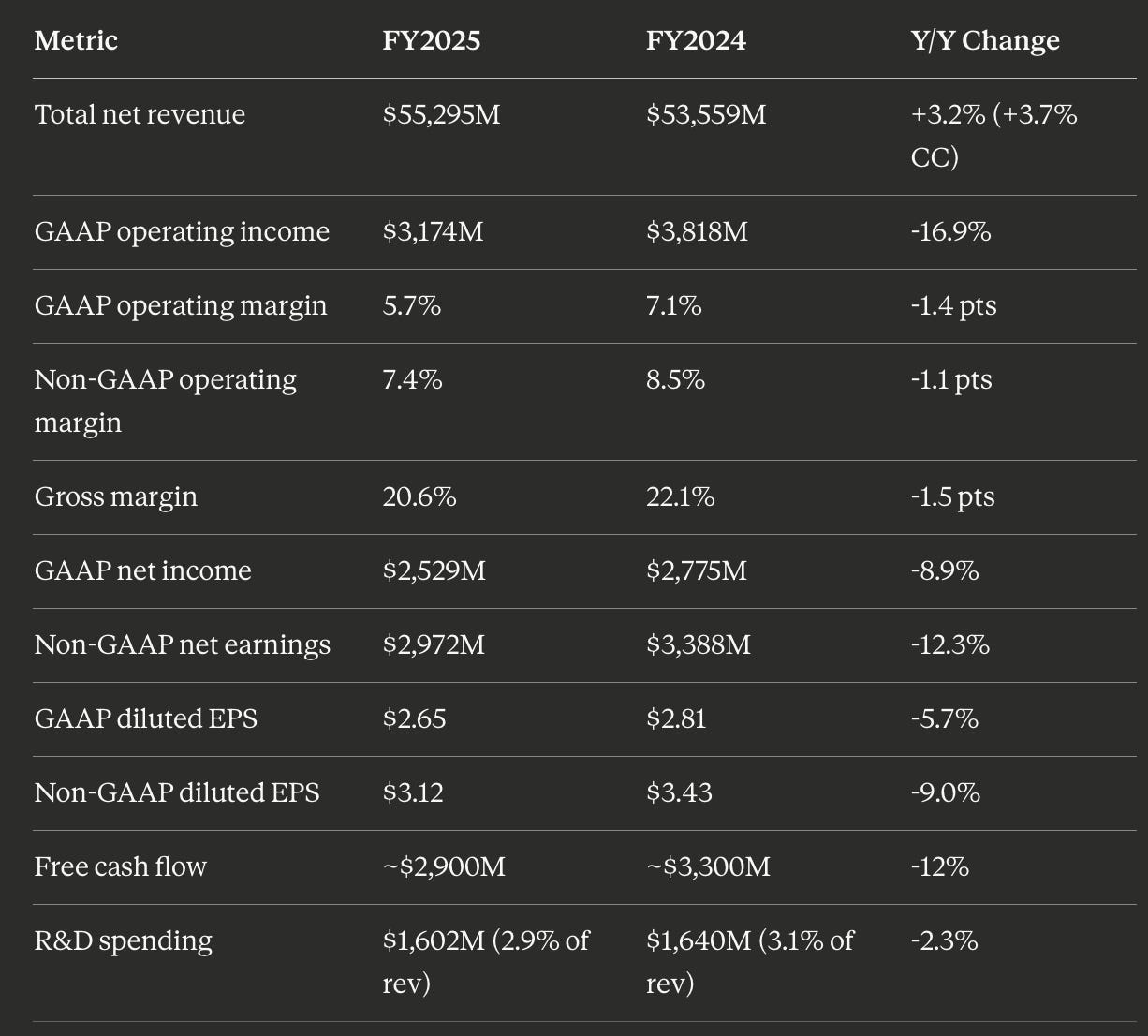

Consolidated results (fiscal year ended October 31, 2025)

Revenue grew but margins compressed meaningfully. Gross margin contracted 150 basis points to 20.6%, driven by tariff costs, component inflation (particularly memory), and manufacturing relocation expenses. Non-GAAP operating margin fell 110 basis points to 7.4%. Free cash flow declined 12% to approximately $2.9 billion, reflecting both lower profitability and higher inventory levels ($8.5 billion, up from $7.7 billion) as HP pre-built buffer stock during the tariff pause.

Segment breakdown

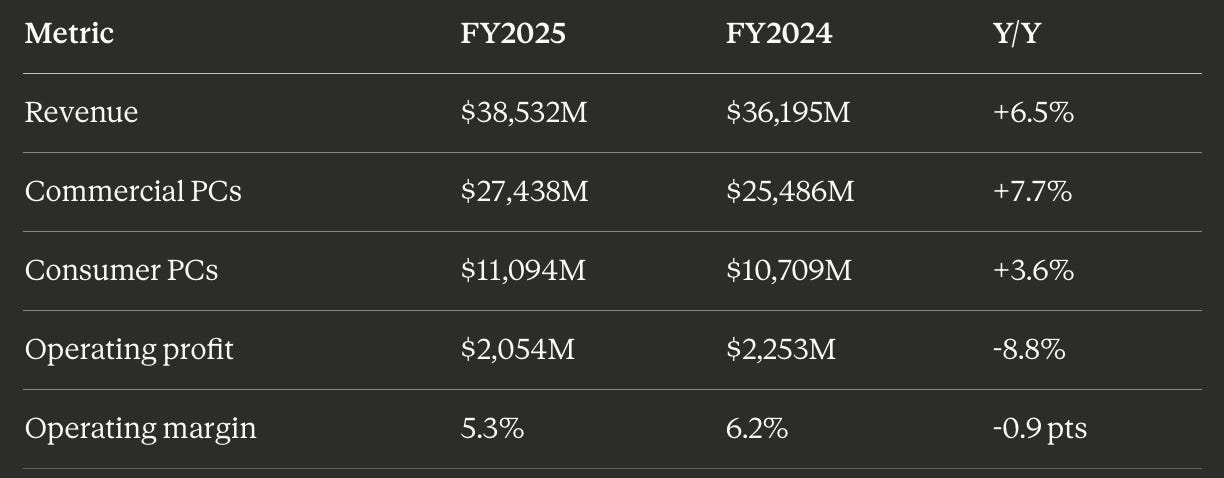

Personal Systems (69.7% of revenue)

Unit shipments rose 4.3% (commercial +6.4%, consumer +1.2%), benefiting from the Windows 10 end-of-life refresh. But the margin story was negative: Personal Systems operating margin fell to 5.3%, the lowest in recent years, squeezed by tariff absorption, competitive pricing, and memory cost inflation. Commercial PCs were the growth engine, consistent with the enterprise refresh cycle dominating the consumer segment.

Printing (30.2% of revenue)

Supplies revenue, at $10.9 billion, represents approximately 65% of total printing revenue and remains the segment’s profit engine. Supplies gross margins are widely estimated at 60%+ by sell-side analysts, though HP does not disclose them separately. The Printing segment’s 18.7% operating margin, while down slightly, remains the highest-margin business at HP by a wide margin and generates more operating profit ($3.1 billion) than Personal Systems ($2.1 billion) despite being less than half its size. Hardware units declined 9% in Q3 and 12% in Q4 FY2025, an acceleration in the rate of decline.

Balance sheet and capital structure (as of October 31, 2025)

HP carries negative book value as a consequence of aggressive share buybacks funded by debt. The balance sheet is a capital return vehicle: accounts payable ($18.1 billion) massively exceed receivables ($5.7 billion) and inventory ($8.5 billion), generating negative cash conversion cycle working capital that funds operations. Net debt of approximately $5.9 billion represents roughly 1.4x EBITDA, manageable but above management’s stated target of under 2x. No goodwill impairment was recorded in FY2025.

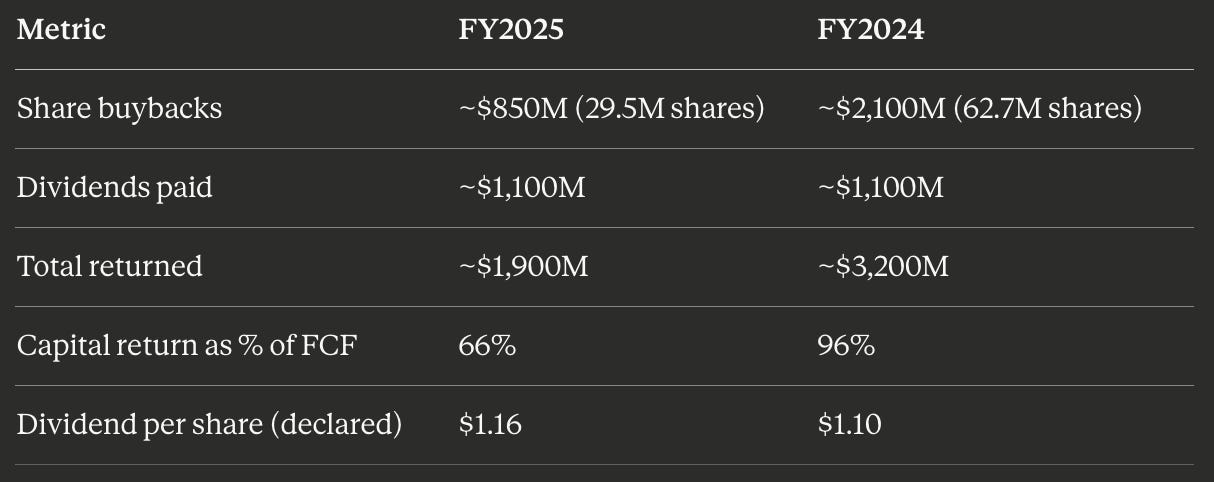

Capital return

Buyback pace slowed dramatically in FY2025, from $2.1 billion to $850 million, partly to fund inventory builds and partly reflecting leverage constraints. The board increased the buyback authorisation to $10 billion in August 2024. For FY2026, the quarterly dividend was raised to $0.30/share ($1.20 annualised), a 3.7% increase, marking the 11th consecutive year of dividend growth. At the current $18.26 stock price, the dividend yield is 6.2%.

Poly acquisition integration

HP acquired Poly (formerly Plantronics/Polycom) for $3.3 billion in August 2023. Original synergy targets were $500 million in revenue synergies and a six-percentage-point operating margin improvement by FY2025. Poly products are now fully integrated into the Personal Systems segment. HP does not separately disclose Poly’s revenue contribution, making it impossible to verify whether the $500 million synergy target was achieved. No goodwill impairment has been taken, suggesting the asset is performing at or near expectations. HP launched Poly VideoOS 5.0 at ISE 2026 with AI noise blocking and smarter camera framing, and is co-developing “HP Dimension with Google Beam” for 3D video communications.

Humane AI acquisition

In February 2025, HP acquired Humane’s AI software platform (”Cosmos”) and 300+ patents for $116 million in cash, a steep discount from Humane’s original $750M-$1B asking price. Humane’s Ai Pin hardware was discontinued. The acquired team formed “HP IQ,” an AI innovation lab. No specific product revenue impact has been disclosed. HP IQ is focused on building a local-first AI software ecosystem with a 20-billion-parameter on-device model. HP also partnered with OpenAI in January 2026 to integrate AI agents into the EliteBook series.

Future Ready restructuring

The Fiscal 2023 “Future Ready” plan, announced November 2022, targeted $1.4 billion in annualised savings, later raised to $1.9 billion by end of FY2025. Cumulative restructuring charges totalled approximately $1.23 billion across FY2023-2025 ($527M + $301M + $405M). The plan delivered approximately $2.2 billion in gross savings, a 1.8x savings-to-charge ratio.

A new Fiscal 2026 restructuring plan was announced November 25, 2025, targeting $1.0 billion in additional gross run-rate savings by end of FY2028, with 4,000 to 6,000 headcount reductions (approximately 7-10% of the 58,000 workforce). Estimated restructuring charges are $650 million, with $250 million in FY2026. The plan emphasises AI adoption to drive productivity.

FY2026 guidance (issued November 2025)

Management guided to the low end of the EPS range, citing approximately $0.30 per share of headwind from memory cost inflation and ongoing tariff-related costs. HP’s Q1 FY2026 (November 2025 to January 2026) came in at $14.4 billion in revenue (+6.9%), with Personal Systems up 11% and Printing down 2%. AI PCs reached 35% of HP’s shipment mix in Q1 FY2026, with a target of 50% by year-end.

2. Market context: the operating environment through March 2026

Global PC market shipments rebounded strongly in 2025

The worldwide PC market shipped approximately 270-285 million units in calendar 2025, representing 8-9% year-over-year growth, according to Gartner (270.2M, +9.1%) and IDC (284.7M, +8.1%). This was the strongest growth since the pandemic boom, driven by three converging forces: the Windows 10 end-of-support deadline (October 14, 2025), AI PC category proliferation, and tariff-related pull-forward demand in the first half. Commercial PCs drove the cycle; consumer lagged at low single-digit growth.

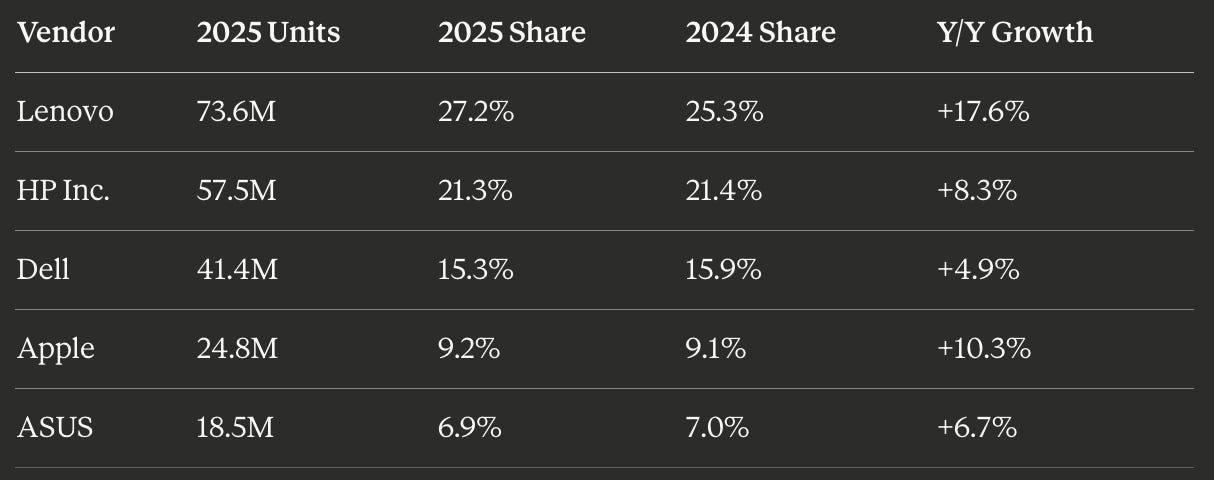

Vendor market share (Gartner, full year 2025)

HP grew below the market average (8.3% vs. 9.1%), losing a marginal 10 basis points of share. Lenovo was the clear share gainer, adding nearly 200 basis points. Dell underperformed at 4.9% growth, losing 60 basis points. Apple outgrew HP at 10.3%. HP remains number one in the United States at approximately 25% share.

AI PC penetration is accelerating but remains uncertain in impact

The AI PC category is ramping quickly, at least on paper. Gartner estimates around 77.8 million AI PCs shipped in 2025, which is roughly 31% of the market. That’s up from 38.1 million units and just 15.6% penetration in 2024. By 2026, the expectation is even more aggressive: 143 million units, crossing the 50% mark to about 55% of all PCs shipped.

What actually defines an “AI PC” is fairly technical. These machines come with a dedicated neural processing unit (NPU) capable of handling 40+ TOPS (trillions of operations per second) of AI workloads. The main chip players are already pushing hard here. Qualcomm’s Snapdragon X Elite/Plus chips deliver around 45 TOPS, Intel’s Core Ultra “Lunar Lake” chips push closer to 48 TOPS, and Advanced Micro Devices (AMD) is around 50 TOPS with its Ryzen AI 300 series. The next wave, expected in 2026, will likely push past 80 TOPS.

HP is clearly trying to stay competitive here. At CES 2026, it showcased its EliteBook X G2 lineup with all three chip options, including a Snapdragon X2 Elite version that reaches around 85 TOPS.

From a business standpoint, AI PCs do help vendors, at least in the short term. They typically sell at a 5–10% premium compared to standard PCs, which lifts revenue per unit. The issue is demand clarity.

On the consumer side, the value proposition hasn’t fully landed. Research from Forrester shows that about half of consumers don’t really understand why they need an AI PC, and 61% don’t think they use AI enough to justify buying one.

Enterprise is a different story. According to International Data Corporation, over 80% of IT decision-makers are planning to invest in AI PCs, which suggests that adoption, at least initially will be driven more by businesses than by everyday consumers.

Windows 10 end-of-life: significant tailwind captured, more remaining

The Windows 10 lifecycle quietly became one of the biggest drivers of the PC market over the last year. Support officially ended on October 14, 2025-but at that point, an estimated 40–50% of the global installed base was still running it.

That’s a massive number when you break it down. Roughly 500 million devices simply can’t upgrade to Windows 11 because the hardware doesn’t meet the requirements. Another 500 million could upgrade but haven’t, either due to inertia, cost, or enterprise-level complexity.

Microsoft has effectively created a buffer to avoid a hard cliff. Through its Extended Security Updates (ESU) program, users can keep receiving security patches until October 2026. For consumers, that costs about $30. For businesses, it’s a stepped structure $61, then $122, then $244 over three years which gradually pushes companies toward upgrading without forcing an immediate shift.

What this has done is stretch the refresh cycle rather than compress it. A lot of the PC demand seen in 2025 was driven by this transition, and that momentum is likely to carry into 2026. The effect is especially pronounced in emerging markets, smaller businesses, and large organisations using ESU as a temporary workaround before committing to a full upgrade.

The 2026 outlook has deteriorated sharply

The PC market just ran into a problem few expected to hit this hard: memory.

International Data Corporation sharply revised its 2026 shipment outlook in Q1, moving from a modest -2.4% decline to a much steeper -11.3%. The driver isn’t demand in the traditional sense, it’s supply pressure coming from somewhere else entirely.

AI datacenters are soaking up huge amounts of DRAM and NAND, effectively crowding out the PC market. That imbalance pushed memory and storage costs up 40–70% between Q1 and Q4 of 2025. For PC makers, that creates a squeeze from both sides: higher input costs and customers who are increasingly price-sensitive.

The result is a tricky trade-off. Vendors are being forced to raise prices, which risks pushing out budget buyers and smaller brands, while at the same time dealing with tighter margins internally.

Interestingly, the overall market value still holds up. IDC expects the PC market to grow slightly, about 1.6% to $274 billion even as unit shipments fall. That tells you what’s really happening underneath: fewer devices being sold, but at higher prices, largely driven by the shift toward more premium, AI-capable machines.

IDC’s framing is pretty telling. This isn’t a short-term blip, it’s the start of a “new normal,” where higher average selling prices become structural, while long-term demand starts to soften.

Printing: structural decline with pockets of resilience

The global hardcopy peripherals market showed modest recovery in H2 2024, with Q4 2024 shipments of approximately 22 million units (+3.1% year-over-year). HP holds 34.2% global printer market share by units, well ahead of Epson (22.5%) and Canon (20.4%). But the trajectory is clear: HP’s Printing segment revenue declined 3.7% in FY2025 to $16.7 billion, with supplies down 3.4% to $10.9 billion. Hardware unit shipments turned sharply negative in the second half (Q3: -9%, Q4: -12%).

Print volumes have not recovered to pre-COVID levels and are not expected to. Quocirca’s 2025 study confirms that 44% of employees work fully remotely or in hybrid arrangements, with this figure expected to reach 51% by 2030. Digital transformation, e-signatures, and cloud storage are permanent headwinds. The decline is primarily structural, not cyclical, though certain verticals (legal, healthcare, education, packaging) maintain stable or growing print needs. The supertank/ink tank printer category is growing at approximately 7% CAGR and directly threatens HP’s razor-blade cartridge model by reducing ink costs to consumers by up to 90%.

HP subscription models in print

HP Instant Ink had approximately 11 million subscribers as of end-2023, the most recent confirmed figure. Revenue is described as approximately $500 million, with management citing a 20% uplift in customer lifetime value when moving from transactional cartridge sales to subscription. HP’s newer All-In Plan, launched in 2024, bundles a printer, automatic ink delivery, and support starting at $6.99/month with a 24-month commitment. HP retains ownership of the printer. Consumer subscriptions collectively reached “just under $1 billion in annual revenue“ with “double-digit revenue growth” and “double-digit sequential subscriber growth,” per the Q4 FY2025 earnings call.

Tariff exposure and supply chain response

The Trump administration’s 2025 tariff regime hit HP hard. Effective rates on China imports peaked at 145%, Vietnam at 46%, and Mexico at 25% for non-USMCA goods. HP’s Chongqing manufacturing hub, built over two decades, was a primary vulnerability. CEO Lores set an initial target of less than 10% of North American products sourced from China by September 2025, then accelerated to “nearly zero China-made products for the U.S. by end of June 2025.”Production shifted to Thailand (consumer laptops), Mexico (commercial notebooks), Vietnam (ramping), India (PCs and printers), and an existing Indianapolis facility. The relocation cost HP $0.12/share in Q2 FY2025 earnings. HP also stopped using the U.S. as a distribution hub for Canada and Latin America to avoid tariff pass-through.

Management claimed tariff costs would be “fully offset by Q4 FY2025” through a combination of supply chain moves and price increases of approximately 5% on PCs. But the FY2026 outlook still embeds tariff-related cost in the guidance, and the situation remains fluid given ongoing trade negotiations.

Among competitors, Dell claims the most diversified supply chain and was more aggressive in passing costs to customers through list price increases. Lenovo faces the steepest challenge due to its deep Chinese manufacturing base; analysts estimated tariff costs could match nearly its entire expected net income for 2025.

3. Financial and valuation lens

HPQ stock: deep value or value trap?

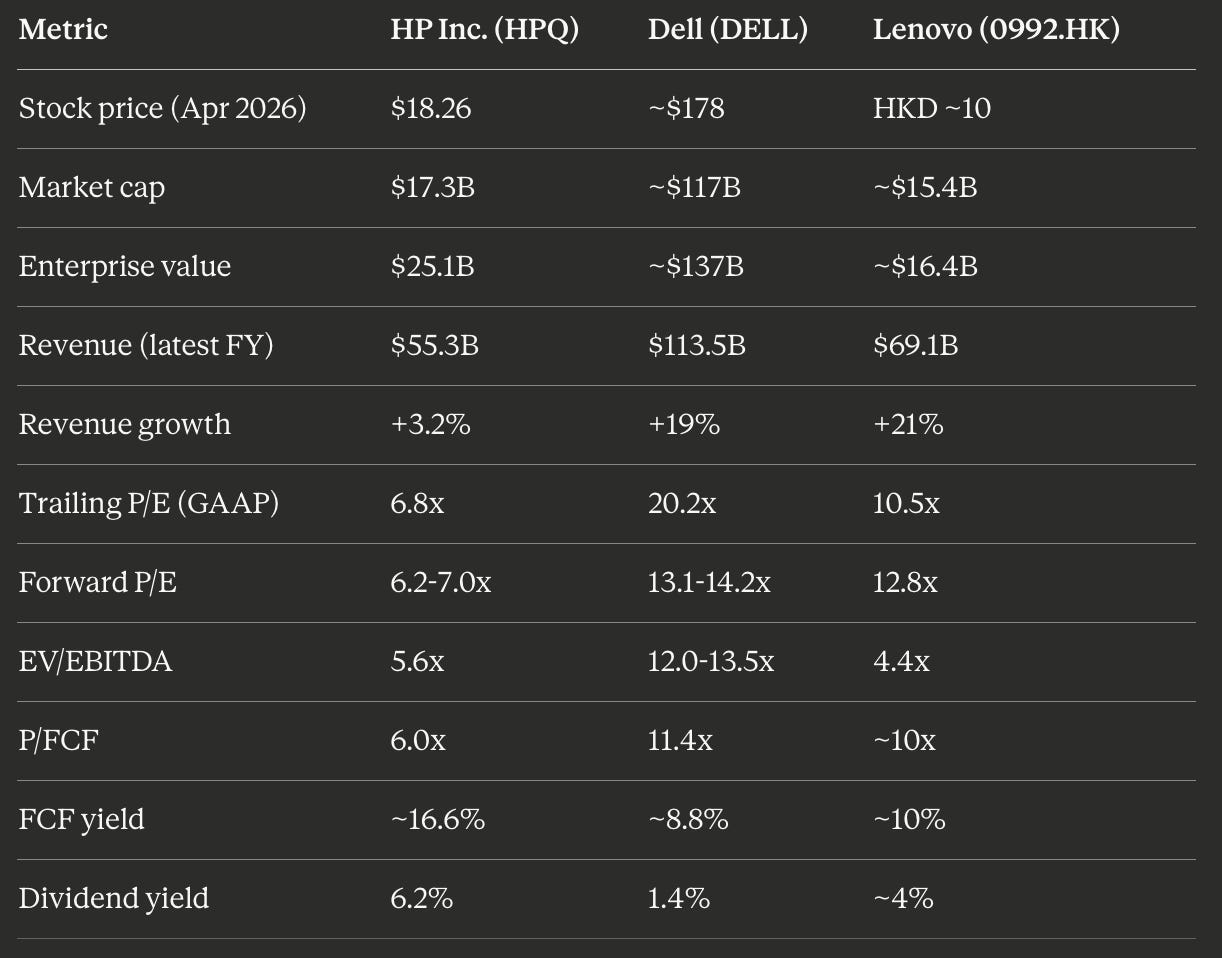

HP trades at roughly one-third of Dell’s P/E multiple and below Lenovo on a forward basis. The stock is 27% below its own 10-year median P/E of 9.5x. It has lost 34-44% of its value over the past twelve months, reaching a 52-week low of $17.56 in early April 2026. Short interest stands at 10.35% of shares outstanding, elevated for a mega-cap hardware name.

The valuation gap explained

Dell’s premium is entirely about AI infrastructure. Dell’s AI server revenue reached $24.7 billion in FY2026 (ended January 2026), up 2.5x year-over-year, with a $43 billion backlog entering FY2027. ISG ($60.8 billion) now exceeds CSG ($51 billion) for the first time, making Dell fundamentally an infrastructure company that also sells PCs. HP has zero AI infrastructure revenue. Its AI narrative is limited to “AI PCs,” which have not yet proven transformative to financial performance.

HP’s further discount versus Lenovo reflects the CEO vacancy (Lenovo has stable leadership), Lenovo’s faster revenue growth (21% vs. 3.2%), and Lenovo’s growing server/infrastructure business ($14.5 billion ISG revenue, +63% in FY2024/25). On EV/EBITDA, Lenovo is actually cheaper than HP at 4.4x, but Lenovo carries lower margins and higher share dilution (shares outstanding increased 13.5% year-over-year).

Capital allocation

HP’s stated policy targets returning approximately 100% of free cash flow to shareholders. In practice, FY2025 returned 66% of FCF ($1.9 billion) as buyback pace slowed to $850 million. The company maintains an $10 billion buyback authorization. M&A capacity is limited: leverage is slightly above the 2x EBITDA target, and the negative equity position constrains the balance sheet optically. HP’s FY2025 total debt of $9.7 billion against $3.7 billion in cash leaves approximately $2-3 billion of M&A headroom before stress-testing credit metrics. Dell, by contrast, generated $8.6 billion in FCF in its latest fiscal year and returned $7.5 billion to shareholders, with a new $10 billion buyback authorization and a $2.10/share dividend (+18% increase).

Analyst sentiment

Consensus is firmly bearish to neutral. TipRanks shows zero buy ratings among 14 analysts (7 hold, 7 sell). StockAnalysis shows an average target of $21.42 (12 analysts), suggesting modest upside from $18.26 but well below the stock’s 52-week high of $29.55. Goldman Sachs carries the most bearish target at $16.00. GuruFocus flags HPQ as a “Possible Value Trap“ despite computing a fair value of $31.56.

4. Strategic issues

The AI PC bet: positioned to participate, not to win

HP has executed well on AI PC product breadth. The EliteBook X G2 series, launched at CES 2026, offers Intel, AMD, and Qualcomm silicon options with up to 85 TOPS NPU performance. AI PCs reached 35% of HP’s Q1 FY2026 shipment mix, with a target of 50% by year-end. HP IQ (from the Humane acquisition) is building an on-device AI system with a 20-billion-parameter local model, and the OpenAI partnership announced in January 2026 brings cloud AI agents to EliteBook.

However, HP’s AI PC position is fundamentally one of participation, not differentiation. The NPU, the core technology enabling AI PCs, comes from Intel, AMD, or Qualcomm. Every PC OEM has access to the same silicon. HP cannot build a silicon moat comparable to Apple’s M-series. The 5-10% ASP premium from AI PCs helps revenue per unit but does not structurally improve margins because HP passes through most of the component cost. Internal studies showing a 16-17% productivity improvement from AI PC deployment are compelling but not unique to HP’s products.

Lenovo holds 31.1% share of the Windows AI PC segment, outpacing HP. Dell ships AI PCs at 55% of its laptop mix. The AI PC category will become table stakes by 2028-2029, with Gartner projecting AI PCs as the norm across the industry. This is not a category where HP can win decisively.

Print decline: structural reality, managed defense

Printing revenue has declined from $17.3 billion to $16.7 billion in one year, and the trajectory is accelerating: hardware units fell 12% in Q4 FY2025. The decline is fundamentally structural. Digital transformation, hybrid work, and sustainability pressures are permanently reducing print volumes, and these forces will not reverse.

HP’s defensive strategy rests on three pillars: (1) subscription models (Instant Ink, All-In Plan) that lock in recurring revenue and increase customer lifetime value by 20%; (2) Dynamic Security firmware that blocks third-party cartridges to protect the supplies annuity; and (3) industrial and commercial print (Indigo digital presses, packaging, 3D printing) targeting growing segments.

The subscription shift is real but still small relative to total printing: consumer subscriptions generate just under $1 billion annually against $16.7 billion in segment revenue. Dynamic Security faces regulatory risk from the EU Right to Repair Directive (effective July 31, 2026), which may restrict HP’s ability to block compatible cartridges. HP has already paid fines in Italy (EUR 10 million) and settlements in the U.S. and Europe over this practice. The supertank printer category (Epson EcoTank, HP Smart Tank) growing at 7% CAGR directly threatens the cartridge model by cutting ink costs 90%.

Industrial Graphics exceeded $1.8 billion in annual revenue with nine consecutive quarters of year-over-year growth. 3D printing showed double-digit growth but remains small (Corporate Investments segment, roughly $43 million in nine months of FY2025). These are legitimate growth vectors, but they cannot offset the $400-500 million annual decline in the core supplies and consumer print business.

Services and subscription transformation

HP’s Workforce Solutions business, anchored by Device-as-a-Service (DaaS) and the HP Workforce Experience Platform (WXP), delivered double-digit growth in FY2025. WXP processes telemetry from 48 million endpoints and manages 2.4 million connected devices. HP was named a Leader in IDC’s MarketScape for Worldwide DaaS 2025. Key growth areas (Workforce Solutions, Consumer Subscriptions, Advanced Compute, Industrial Graphics) collectively represented approximately 20% of total revenue in FY2025.

CFO Karen Parkhill framed the strategic direction explicitly: “We’re excited to drive even greater growth and value in the future with revenue that is less cyclical and more stable and higher margins, focused on driving more recurring revenue.” This is the right direction, but the transition is gradual. HP does not break out Workforce Solutions revenue separately, and the 20% key growth areas figure includes multiple categories. Compared to Dell’s much larger enterprise services operation, HP’s services transformation is nascent.

Hybrid work and Poly

The Poly integration appears operationally successful. Products are deeply embedded in the HP portfolio: Poly Lens Desktop is pre-installed on select HP laptops, and Bluetooth direct technology enables dongle-less headset pairing. The Poly VideoOS 5.0 launch at ISE 2026, built on Android 13 with a support runway through 2032, positions HP’s video conferencing hardware for the long term. The “HP Dimension with Google Beam” co-development suggests HP is investing in next-generation collaboration beyond conventional video.

However, $3.3 billion is a significant investment for what remains a component of the Personal Systems segment without separately disclosed revenue. The hybrid work hardware market is competitive (Logitech, Jabra, Cisco, Microsoft) and cyclical. Whether Poly ultimately justifies its acquisition price depends on cross-selling into HP’s installed PC base, an opportunity that is plausible but unproven at reported scale.

Gaming: present but not a needle-mover

HP’s OMEN brand and HyperX peripherals (acquired from Kingston in 2021 for $425 million) are positioned in mid-to-high-end gaming. HP describes the HyperX acquisition as “now paying dividends,” with the audio and peripheral expertise feeding back into OMEN PC design. However, HP does not disclose gaming-specific revenue or market share, making it impossible to assess its true contribution. Gaming falls within Personal Systems and competes against strong dedicated brands (Alienware/Dell, ASUS ROG, MSI, Razer). The gaming PC market stabilized in 2025 after headwinds in 2023-2024, boosted by Nvidia RTX 50-series launches. For HP, gaming is a profitable niche within the premium consumer category but is unlikely to meaningfully alter the company’s financial trajectory.

Management transition

Enrique Lores departed as CEO on February 2, 2026, leaving to become CEO of PayPal after approximately 6.3 years at the helm. He joined HP as an intern 36 years ago. Bruce Broussard, age 63, a board member since 2021 and former Humana CEO, was appointed interim CEO effective February 3, 2026. He receives $362,500/month in cash and a $7 million RSU grant vesting in February 2027. A CEO Search Committee has been formed with a global search firm engaged.

Board Chair Chip Bergh (age 68, former Levi Strauss CEO, Harvard Business School lecturer) leads a 12-member board. Four new independent directors have been added since early FY2024, including Songyee Yoon (managing partner at Principal Venture Partners, AI/tech expertise). Say-on-pay received over 91% approval in 2024. No activist investor involvement is currently flagged.

The CEO vacancy is a meaningful overhang. The Investor Day has been delayed. The incoming CEO will need to decide how aggressively to restructure the printing business, whether to pursue transformative M&A (e.g., in AI infrastructure or software), and how to reposition HP’s narrative in a market that is only rewarding AI infrastructure stories. Broussard’s healthcare background provides operational discipline but no obvious technology vision.

5. Competitive and structural risks

Lenovo’s scale advantage is widening. Lenovo shipped 73.6 million PCs in 2025 to HP’s 57.5 million, a 16-million-unit gap, and grew 17.6% versus HP’s 8.3%. Lenovo has 30+ manufacturing facilities in nine markets, holds 31.1% share in Windows AI PCs, and is growing its ISG server business 63% YoY. Its Chinesecost base is a double-edged sword (tariff exposure) but provides structural cost advantages in non-U.S. markets.

Dell’s AI infrastructure halo is the most significant competitive dynamic. Dell’s $43 billion AI server backlog and $24.7 billion in AI server revenue in FY2026 create enterprise relationships that extend to PC procurement. Dell’s ISG now exceeds its CSG in revenue, fundamentally repositioning the company away from pure PC/print competition. This gives Dell a valuation premium, a growth narrative, and enterprise bundling opportunities HP cannot match.

Apple’s silicon moat in the premium segment is unassailable. Apple captures over 53% of total laptop revenue on Amazon U.S. despite lower unit volumes. M-series chips deliver superior performance-per-watt that HP, dependent on Intel/AMD/Qualcomm, cannot replicate.

Commoditization is the baseline condition. The top three PC vendors hold 61% of the global market, operating on the same Windows platform with the same Intel/AMD/Qualcomm components. HP’s PC operating margin of 5.3% reflects this reality. AI PC features have not yet created meaningful differentiation because the AI silicon is available to all OEMs.

Print cartridge erosion comes from multiple vectors: aftermarket cartridges (50-80% cheaper than OEM), the supertank/EcoTank category (90% lower ink costs), and the EU Right to Repair Directive (effective July 2026). HP’s Dynamic Security strategy, which blocks third-party cartridges via firmware, faces increasing regulatory and reputational risk. Italy’s EUR 10 million fine and the U.S. class action settlement are precedents, and EU Right to Repair may fundamentally challenge the practice.

Memory cost inflation is an acute near-term risk. DRAM and NAND prices rose 40-70% in 2025 as AI datacenter demand consumed available supply. HP guided to a $0.30/share EPS headwind in FY2026 from memory costs alone. IDC projects memory shortages persisting through 2027.

Tariff uncertainty remains. HP’s rapid supply chain diversification (targeting near-zero China manufacturing for U.S.-bound products by mid-2025) mitigates the immediate exposure, but production in Vietnam (46% tariff) and evolving trade policy create ongoing risk. HP’s relocation costs compress near-term margins even as they reduce long-term tariff exposure.

6. Strategic recommendations and the honest cases

What HP should double down on

Workforce Solutions and DaaS: This is HP’s best path to a recurring-revenue, higher-margin business model. The WXP platform at 48 million endpoints has real scale. HP should invest aggressively in expanding managed services, AI-driven device management, and bundled PC-as-a-service offerings for enterprise customers. The goal should be to grow this from approximately 20% of revenue to 35%+ within five years.

Print subscription acceleration: Consumer subscriptions at just under $1 billion are working but growing too slowly relative to the $10.9 billion supplies base that is declining 3-4% annually. HP should consider more aggressive pricing (lower monthly fees) to drive adoption volume, accepting near-term revenue headwinds for long-term annuity value. The All-In Plan’s bundled hardware model is strategically sound and should be expanded internationally and into commercial accounts.

Industrial print and packaging: The $1.8 billion Industrial Graphics business with nine consecutive quarters of growth is HP’s most underappreciated asset. Packaging, labels, textiles, and on-demand book printing are structural growth segments as e-commerce, SKU fragmentation, and premiumisation drive demand. HP Indigo’s digital press leadership and the expanding 3D printing portfolio (Metal Jet, Multi Jet Fusion, new filament systems in 2026) deserve more capital and attention.

What HP should consider exiting or restructuring

Consumer print hardware: With units declining 9-12% per quarter, consumer printer hardware is approaching a phase where HP should manage for cash rather than growth. The All-In Plan, where HP retains printer ownership, is the right model, effectively converting a product sale into a service. But standalone consumer printer hardware sales at progressively lower volumes and margins should be rationalised.

M&A moves worth considering

HP’s M&A capacity is limited (approximately $2-3 billion before stressing credit metrics), constraining transformative deals. Within that envelope, HP should consider: (1) acquiring a managed services or IT services firm to accelerate the Workforce Solutions buildout; (2) acquiring collaboration software assets to complement Poly hardware with recurring software revenue; (3) selectively acquiring industrial print or packaging technology to strengthen the fastest-growing print subsegment. HP should avoid large, dilutive hardware acquisitions. The Poly deal stretched the balance sheet, and another deal of that scale is inadvisable without first deleveraging.

Capital allocation priorities

At the current $18.26 share price and 16.6% FCF yield, share buybacks are extremely accretive and should be the primary capital return mechanism. HP’s stock is likely undervalued on a fundamental basis, though the “value trap” risk is real if earnings continue declining. HP should target returning 80-90% of FCF through buybacks and dividends, with the remainder reserved for tuck-in M&A and working capital needs. The current 66% payout ratio (FY2025) should increase once the tariff-related inventory builds normalise.

The honest bull case

HP trades at 6.8x earnings and a 16.6% free cash flow yield with a 6.2% dividend yield, all supported by a $10.9 billion supplies annuity. The Windows 10 refresh cycle extends into 2026-2027, providing PC volume support. AI PC ASP premiums of 5-10% structurally improve revenue per unit. The new restructuring plan should deliver $1 billion in savings by FY2028, supporting earnings even if top-line growth stalls. Subscription revenue is approaching $1 billion and growing double digits. The incoming CEO could accelerate strategic transformation. At this valuation, HP does not need to become a growth stock; it merely needs to stabilise earnings and maintain its capital return, delivering a 15%+ total return through yield and buybacks alone.

The honest bear case

HP is a declining-margin hardware business with no AI infrastructure story, a departing CEO, and structural headwinds in its highest-margin segment (printing). The PC business operates at 5.3% margins in a commoditized market where the company is losing share to Lenovo. Memory cost inflation, tariff volatility, and EU regulatory risk on printer cartridges create compounding margin pressures. The FY2026 EPS guide of $2.90-$3.20 implies further earnings decline. The $10.9 billion supplies business is declining 3-4% annually with no credible path to stabilization. The AI PC narrative is shared by every OEM and provides no competitive moat. The stock is cheap because the business is getting worse, and it may keep getting cheaper. Zero of 14 sell-side analysts rate the stock a buy.

Key data flags and uncertainties

The following data points carry meaningful uncertainty and should be verified against HP’s FY2025 10-K and 2026 Proxy (primary source document referenced by the user):

Poly revenue contribution: Not separately disclosed; synergy achievement unverifiable from public filings.

Instant Ink subscriber count: Most recent confirmed figure is 11 million from end-2023; current count likely higher but undisclosed.

Supplies gross margin: Widely cited at 60%+ by analysts but not disclosed by HP; segment operating margin of 18.7% is the reported metric.

Workforce Solutions revenue: Described qualitatively as “double-digit growth” but absolute figure not disclosed separately.

Remaining buyback authorization: Estimated at $7-8 billion but exact figure requires proxy verification.

Net debt: Ranges from $5.9 billion (FY2025 year-end) to $7.8 billion (Q1 FY2026 TTM) depending on reference date and debt definition.

2026 PC market outlook: IDC’s -11.3% forecast was a sharp March 2026 revision from -2.4% in November 2025, reflecting the fast-moving memory crisis; this figure may be revised again.

Gaming revenue: Not separately disclosed by HP; impossible to assess true financial contribution.

CEO search timeline: No public indication of when a permanent CEO will be named.

Found this valuable, do share it ahead!